By Evy Hambro, BlackRock World Mining

The mining sector appears much more stable after experiencing a prolonged period of negative growth. Things had looked promising at the start of 2015 but the second half of the year saw a significant sell-off in shares. The sector fell by 36% at that time - caused by fears about a sharp slow-down in China, combined with concerns about mining companies’ debt levels[i]. However, the start of 2016 saw mining rally strongly and it is now back to the levels that we saw in the first half of 2015. Several factors have contributed to this resurgence.

One such factor is that mining companies have reduced their debt significantly – they have sold assets and generated more business. Investors are still light in the sector as a result of the second half of 2015, but commodity prices are rising and costs are lower. We do not believe we will return to the lows from last year, though mining shares can be volatile, and investors should keep this in mind.

There are three main reasons we could see dividend growth from mining companies.

Firstly, if and when the major mining companies pay dividends, they do so in US dollars. As a result of sterling’s recent depreciation, the dividend growth for UK investors will be significant, even if payments stay flat. However, there is always the chance that the currency could have moved against us since currencies are volatile and their strength or weaknesses change all the time.

Second, a number of companies cut their dividends to preserve flexibility on their balance sheet during weaker points last year. Now they are in a better position, they can improve dividend payouts.

Finally, some companies removed dividends totally, and we believe it is likely those companies will re-establish payments. For example Glencore, which has not paid a dividend since September 2015[ii], has said it may resume dividend payments in 2017[iii].

After prolonged periods of under-investment by commodity companies – as we have seen over the past four years – there follows a lack of supply. Capital investment peaked in 2012 after which expenditure by commodities companies has fallen, which is taking some mined commodities from surplus into deficit. In response, we are gradually seeing prices rise. However, the Trust doesn’t look at prices in isolation; we also look at the value of shares. We will only invest if we identify a combination of attractive commodity prices and attractive valuation of shares.

We have been building our exposure to gold and silver over the past few years which has enabled us to benefit from strong performance and, in particular, higher gold prices, pushed up by increasing demand for the yellow metal. We only hold high-quality gold companies with strong management track records, such as Fresnillo and Avanco[iv], so we underperformed the gold index while investors rushed to companies in which we chose not to invest. That said, we didn’t stray from our investment process or follow the herd and, by continuing to hold quality companies, we are getting that performance back.

China is the world’s leading producer of coal and gold, and the world’s leading consumer of most mining products, so there’s no doubt the sector has been affected by fears about its slowing GDP growth. In the second half of last year there was an incredibly strong negative sentiment towards China. However, this year the fears on China have receded and investors seem more comfortable with the direction in which Chinese fiscal policy - meaning questions of taxation and public spending - is travelling[v].

----------------------------------------

[i] 30/06/15 – 14/12/15, Datastream, sterling terms, represented by the Euromoney Global Mining Index, November 2016 [ii] DividendMax, November 2016 [iii] Bloomberg.com, March 2016 [iv] BlackRock, September 2016 [v] Bloomberg, September 2016

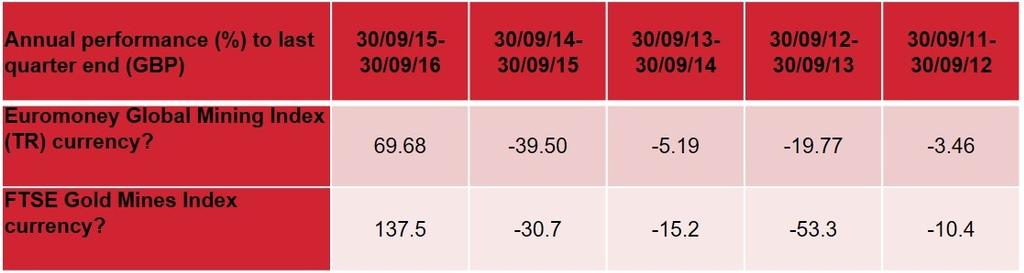

The Euromoney Global Mining Index performance figures are based on total returns net of taxes and dividends, with income reinvested. The FTSE Gold Mines Index performance figures are based on capital appreciation only. Past performance is not indicative of current or future results and should not be the sole factor of consideration when selecting a product. It is not possible to invest directly into an index.