A series of independent reviews have made strident recommendations about how to reduce the dominance of the ‘big four’ audit firms, strengthen the quality of audits and give teeth to the regulator.

Changes have been debated before, but this time it is different. The strength of political will is likely to result in substantial change to how audits are tendered, conducted and reported.

Most recently MPs have recommended:

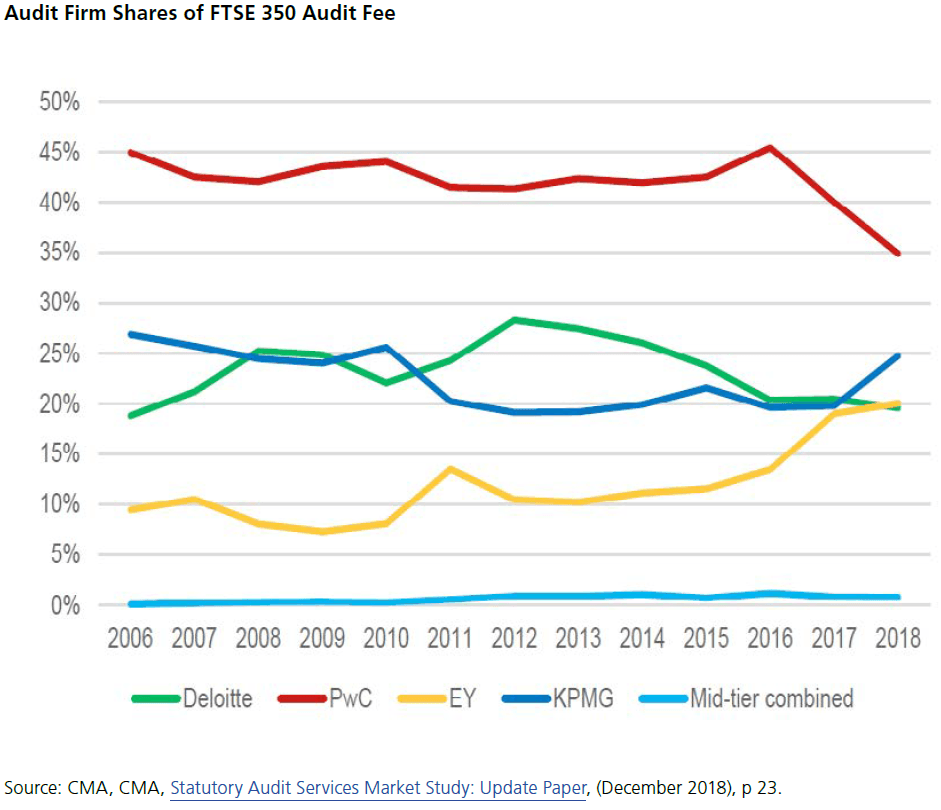

The lack of competition in the audit market and the dominance of the ‘big four’ has also raised concerns among MPs.

They want more choice and higher quality audits. MPs propose piloting mandatory joint audits where auditors share the work, and both sign the audit opinion. This could allow smaller firms to grow, be more competitive and get more experience of FTSE 350 audits. But views are polarised, with some citing that there is little evidence that joint auditors improve audit quality, independence or choice.

Another approach being considered is introducing a cap on market share for the ‘big four’. This may give mid-tier firms a chance to increase their proportion of FTSE 350 audits.

To speed up any change in the audit market it is also possible that auditors will be required to rotate more frequently. Audit appointments may potentially be limited to seven-year periods which could not be renewed.

Further recommendations have also been made which will impact audit committees, including regulatory scrutiny of the committee and making all directors, regardless of their professional qualifications, accountable for their performance and liable to the regulator’s sanctions.

The AIC argues that any reforms should be proportionate, recognising that investment company audits are simpler than large, multinational trading companies. Undoubtedly, if these rules are introduced they may affect member options. In the short term, the choice may become more limited, particularly if the ‘big four’ are unable or unwilling to respond to tenders if they are concerned about a possible market cap.

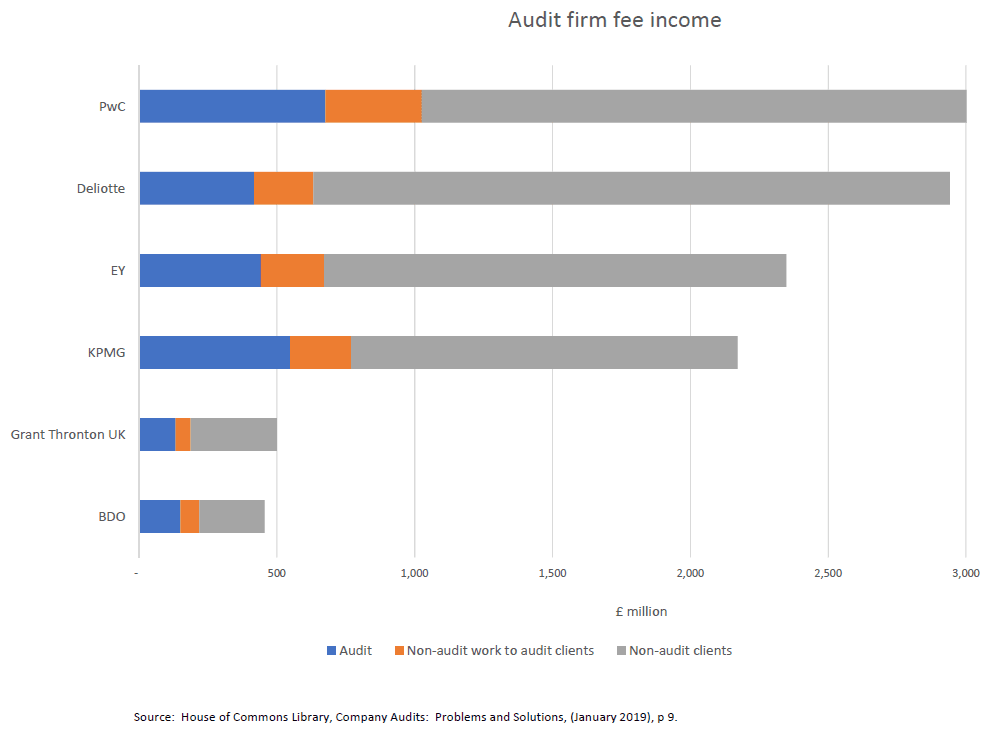

Audit firms are already considering how to stave off the worst-case scenario. Some are looking at moving their audit practices into separate subsidiaries in the hope that this will help prove their independence. But their non-audit business is significantly larger.

Further consultations will be held to develop specific proposals, but it is clear that the direction of travel has been set and all parts of the audit process will face new challenges.