When it comes to providing exposure to illiquid assets, investment companies are an obvious choice. They are immune to the problems that accompany open-ended funds holding illiquid assets when meeting high levels of redemptions.

The fragility of the open-ended approach was exposed by the market uncertainty that arose from the 2016 Brexit referendum result where nervous investors made high levels of redemption requests leading to the suspension of a number of funds. It is understood that eight open-ended funds were suspended in the period following the Brexit vote compared with zero investment companies. In contrast, holders of investment company property shares were able to trade after the Brexit vote.

The markets have since stabilised but perhaps the threat has not passed. Just recently, Moneyweek foretold dire consequences for the open-ended property fund sector, predicting ‘a worse crisis than the crash of mid-2016’. Clearly some funds are more suited to holding illiquid assets than others. But these are facts which appear to have passed the regulator by.

New measures proposed by the Financial Conduct Authority (FCA) are aimed at increasing consumer protections in relation to open-ended funds which invest in illiquid assets. Under the proposals, “Funds Investing in Illiquid Assets” (FIIAs) would have to suspend if there is material uncertainty about asset values. Other rules seek to improve liquidity risk monitoring and management and increase transparency.

For the most part, these are sensible proposals (although it is possible that they may result in more frequent suspensions). But in addressing the issue, the regulator has focused on propping up an unstable structure rather than clearly promoting better alternatives, such as investment companies.

The regulator doesn't seem to have appreciated the obvious advantages investment companies offer over open-ended funds when investing in illiquid assets:

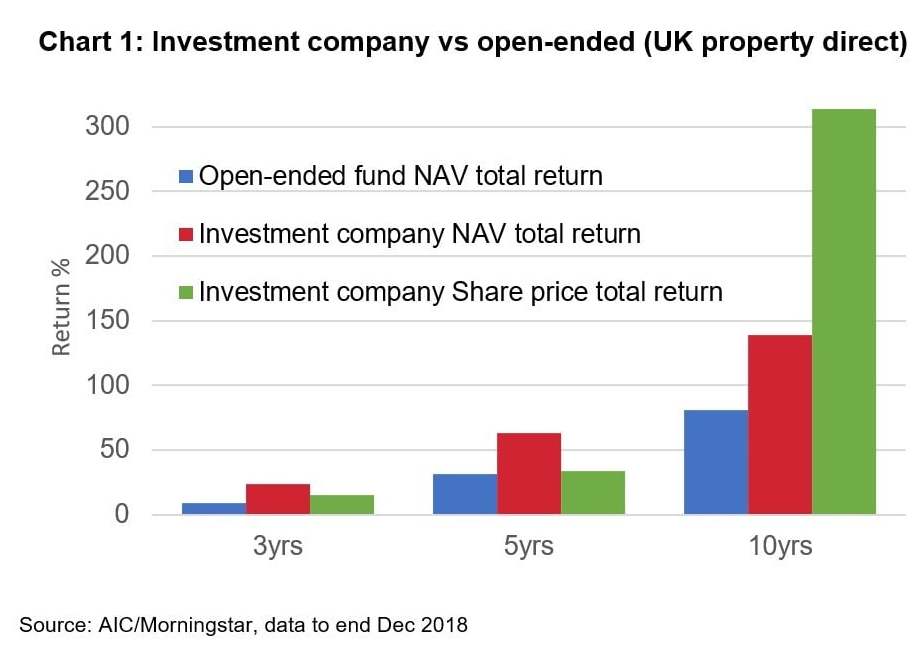

As well as being structurally robust, this allows investment companies holding illiquid assets to offer superior returns (See Chart 1). A key reason for this being that investment companies are not hampered by the need to retain a significant cash holding (currently running at an average of 20% in the open-ended fund sector) to finance redemptions.

The FCA’s starting point for discussing access to patient capital investments is focused primarily on funds within the authorised regime such as UCITS, NURS, and QISs. There is little indication that it is currently considering other measures to ensure a competitive market exists for all products offering (arguably superior) access to illiquid assets.

While the FCA has recognised benefits of encouraging and facilitating investment in illiquid assets, its focus has been too narrow. The AIC has called for a more expansive approach, urging the regulator to see investment companies as part of the solution to allowing a wider range of investors to access the benefits of patient capital.

Reports that the regulator is actively monitoring open-ended property funds’ liquidity, because of concerns about volumes of redemptions as Brexit uncertainty continues, justify this view. Hopefully, the FCA will shift its stance to accommodate what is obvious to champions of the investment company sector.