Guy Rainbird discusses the challenging issue of 'overboarding'

Guy Rainbird, Public Affairs Director

‘Comply or explain’ governance promises flexibility and high standards. These laudable objectives often flounder when reality bites. It is a huge challenge to design broadly-applicable, practical systems able to take account of the different circumstances of companies and their boards. Because of this, investors often follow general policies which are less flexible than many would hope. A case in point is the question of whether an individual director has enough time to devote to their role or whether they are ‘overboarded’.

Best practice says directors should have “sufficient time to meet their board responsibilities”. How this principle should be interpreted is, for the most part, left open. The Financial Reporting Council, which sets standards in this area, offers guidance only to the extent that “full-time executive directors should not take on more than one non-executive directorship in a FTSE 100 company or other significant appointment.” Otherwise, that’s it.

At one level this is sensible. This question is a matter of judgement and depends on specific circumstances. It is nonetheless a challenge for investors to understand, and take a view on, the position of, potentially, thousands of individual directors on hundreds of boards.

One approach is to apply a numerical formula to board appointments. While variations on this theme exist, perhaps the best-known approach is that of Institutional Shareholder Services (ISS). Its policy includes a scoring system specifying that individuals should not have positions which accrue, in total, more than five ‘mandates’. Each listed company directorship is counted as one mandate. The role of ‘chair’ is counted as two mandates.

This approach is clearly convenient but, at first sight, also has significant drawbacks. Its focus arguably penalises those with a portfolio of listed company directorships while not taking so strict a view of those with other private or charitable interests. There is no obvious differentiation between the time taken to discharge a role on a complex trading company (perhaps one with multinational interests, complex organisational structures and significant operational risks) compared with the potentially less onerous requirements of an investment company with a more narrowly focussed oversight agenda.

Fortunately, the risks of these formulaic approaches can be mitigated. Feedback from various agencies and investors with ‘points-based’ systems is that these limits are not as inflexible as they may seem.

There is recognition that investment company directorships can be less time-intensive than other listed company roles. Where adequate information is provided some agencies and investors can be persuaded that breaching their policy’s points limit need not always disqualify a director from taking up an additional position. The key to achieving a sympathetic hearing is setting out in the annual report an explanation of the commitments of the individual and why the board considers that they have the capacity to undertake the role. This explanation should go further than stating that the board believes an individual has enough capacity. Where more information has been provided, directors with non-executive investment company portfolios have reported being able to secure additional positions without attracting negative recommendations and votes. This is a challenging issue, but evolving practice indicates that greater transparency, potentially alongside engagement, can overcome some of the downside of governance formulae. Certainly, not providing clear explanations raises the risk that the numbers alone will govern investor views and votes.

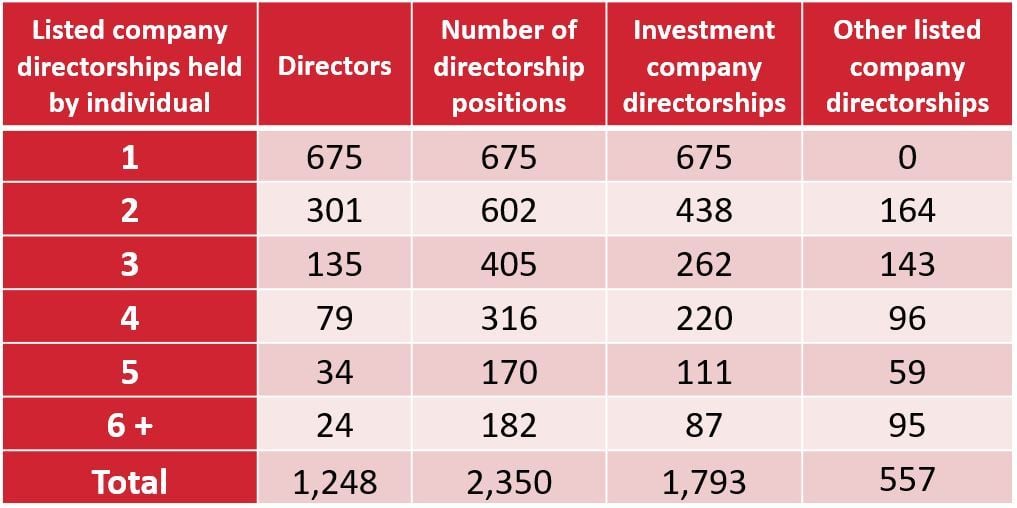

Listed board positions of investment company directors. Source - BoardEx

Guy Rainbird Public Affairs Director T: 020 7282 5553 E: Guy.Rainbird@theaic.co.uk