Faith Glasgow explores whether investment company size matters

It seems that big is increasingly beautiful for investment companies (ICs). Over recent years, there has been growing pressure on them to become larger and more liquid, and the most successful companies now have net asset values (NAVs) in the billions of pounds.

Scottish Mortgage, by far the largest, has a NAV of around £17 billion, but Alliance Trust, F&C, Monks, RIT Capital Partners, Polar Capital Technology, Greencoat UK Wind, The Renewables Infrastructure Group, Tritax Big Box and Pershing Square Holdings all have NAVs above £3 billion, and there are around 50 more ICs with NAVs of between £1 and £3 billion.

Why should size be considered advantageous? Most obviously, greater market capitalisation provides greater liquidity, which makes it easier for large wealth managers – where so much IC investment is now concentrated – to deal successfully.

As Priyesh Parmar, associate director at broker Numis, explains: “Trading liquidity is one of the most challenging issues facing the investment companies sector, particularly as wealth managers have consolidated in recent years and make increasing use of centralised buy-lists.”

Andrew McHattie, in his excellent new book Investment Trusts – A Complete Guide, puts it succinctly: “For wealth managers and institutions needing to deal in larger blocks of shares, it can be extremely frustrating if the normal dealing size is too small to accommodate those needs.”

Source: AIC/Morningstar, data end Feb

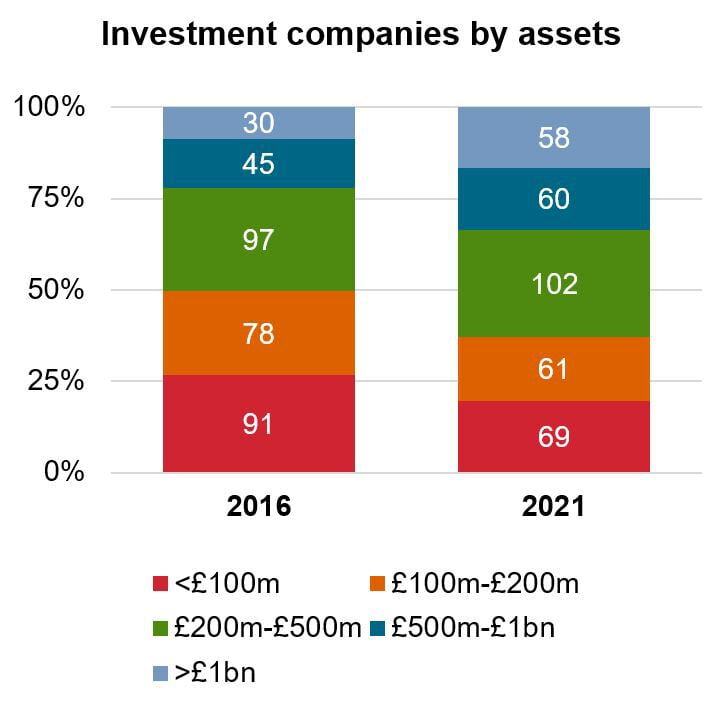

McHattie points out that in 2010 the minimum size of trust workable for a wealth manager was considered to be £50 million; now it is £200 million. Yet around 45% (by number) of the closed-ended universe of around 400 companies are worth less than £200 million, according to Numis.

Such small investment companies never make it on to the radar of most of the institutional investors, and many are trading on wide discounts as a consequence.

There are further benefits to being big. Large companies can tap into economies of scale as they’re able to spread fixed costs – such the fees for auditors and directors or the printing of the annual report – over a larger asset base. Dealing spreads also tend to be smaller for larger, more liquid and more widely traded companies. Again, smaller, relatively illiquid peers lose out.

The upshot is that big, successful companies tend to get bigger, while those small funds “that are undifferentiated from their peers and limited in scale need a strategy for growth or improvement if they are to survive", according to Numis’s Ewan Lovett-Turner. Some boards have simply wound up in the face of that pressure: AIC data shows 20 companies were closed in 2020.

But not all small investment companies are anxious to grow. For those investing in niche areas with limited investment capacity, such as micro caps, there can be disadvantages in being too large.

The best example of 'deliberate smallness’ among the handful of micro cap ICs is River & Mercantile UK Micro Cap (RMMC), which runs a concentrated portfolio of around 40 companies and has limited its size to £100 million ever since its IPO in 2014.

George Ensor, manager of the company, sets out the rationale behind this approach: “Contrary to both the broader trend for larger trusts and the commercial incentive of running a larger trust, the size of RMMC is limited because we believe it will enable us to deliver higher returns to shareholders.

“We look to invest in a part of the market – companies with a market capitalisation of less than £100 million – which is often overlooked by others. It is challenging for larger funds to gain significant exposure to these micro-cap companies. The constraint on the size of the trust is really a result of the size of the companies we are investing in and the number of holdings we have, as running a larger trust would require a less concentrated portfolio (i.e. more holdings).”

RMMC returns capital to shareholders through a compulsory partial redemption of shares when the trust gets too large; that has happened four times since listing, most recently in January this year. “It is a very cost-effective method, and we have returned approximately £57 million of the £70 million that has been raised since IPO back to shareholders,” adds Ensor.

While RMMC is the only trust to actively cap its growth, Miton UK Microcap, run by Gervais Williams, has an annual redemption option, whereby shareholders can choose to redeem some or all of their shares for cash.

Other trusts with a niche focus may also prefer to limit their size: McHattie reports that “the manager of BlackRock Frontiers (BRFI), which invests in some small, out-of-the-way markets such as Kazakhstan and Kenya, has also spoken of a maximum size for efficient investment”.

Killik’s head of managed portfolio services Mick Gilligan suggests that restrictions on size may also be beneficial to avoid issues of dilution. Possible examples include trusts that hold a very rare and valuable set of assets, where further capital raises risk diluting the quality (possibly venture capital trusts), or those where the running yield is very attractive and fresh capital could not be deployed at similarly attractive yields.

“Tritax Big Box is a possible example of a vehicle where consecutive capital raises in a tight market were invested at progressively lower yields,” Gilligan adds.

There is a further aspect to this whole issue of the attractions of size. As mentioned earlier, small, under-the-radar investment companies may in many cases be trading on hefty discounts -– and one multi-manager IC in particular has successfully focused its attention on sniffing out those offering unrecognised opportunities.

“Miton Global Opportunities (MIGO) has a unique mandate within the sector through its focus on exploiting pricing inefficiencies among closed-ended funds,” says Parmar.

The managers Nick Greenwood and Charlotte Cuthbertson seek funds that have fallen out of favour and trade on wide discounts. “With many smaller trusts falling below the radar of wealth managers, and in particular given the growth of alternative asset classes, there is a lot of scope for mispricings,” they comment.

MIGO has a NAV of only £89 million, but has had an outstanding run, with NAV growth up 61% over one year and more than doubling over five. That suggests there are clearly hidden gems within the lower ranks of the closed-ended universe; it’s just a matter of knowing how to find them.

Ultimately, though, Gilligan believes that in general the pressure to grow is almost irresistible in the closed-ended universe: “I suspect most trusts would like to grow, even those in small cap sectors; I don't think many, if any, illiquid small cap trusts are the size they are out of choice.”