by Nick Britton

Nick Britton

As I write this, my kids are raising havoc downstairs. My wife is on a crucial conference call and in about 20 minutes I need to start thinking about making the dinner – although it feels like we only just had lunch.

Such is lockdown, which has changed all our lives so radically that it feels like we are living in a particularly unexciting zombie film. Of course, those of us with jobs we can do safely ensconced in our homes, while remaining safe and healthy, are the lucky ones. But it’s hard to remember that, when the experience of home-schooling your children brings you face-to-face daily with your own inadequacies. My CPD may be accredited by the CII and CISI, but it turns out I am pretty useless at Key Stage 1, where there’s surprisingly little focus on the pros and cons of the closed-ended structure.

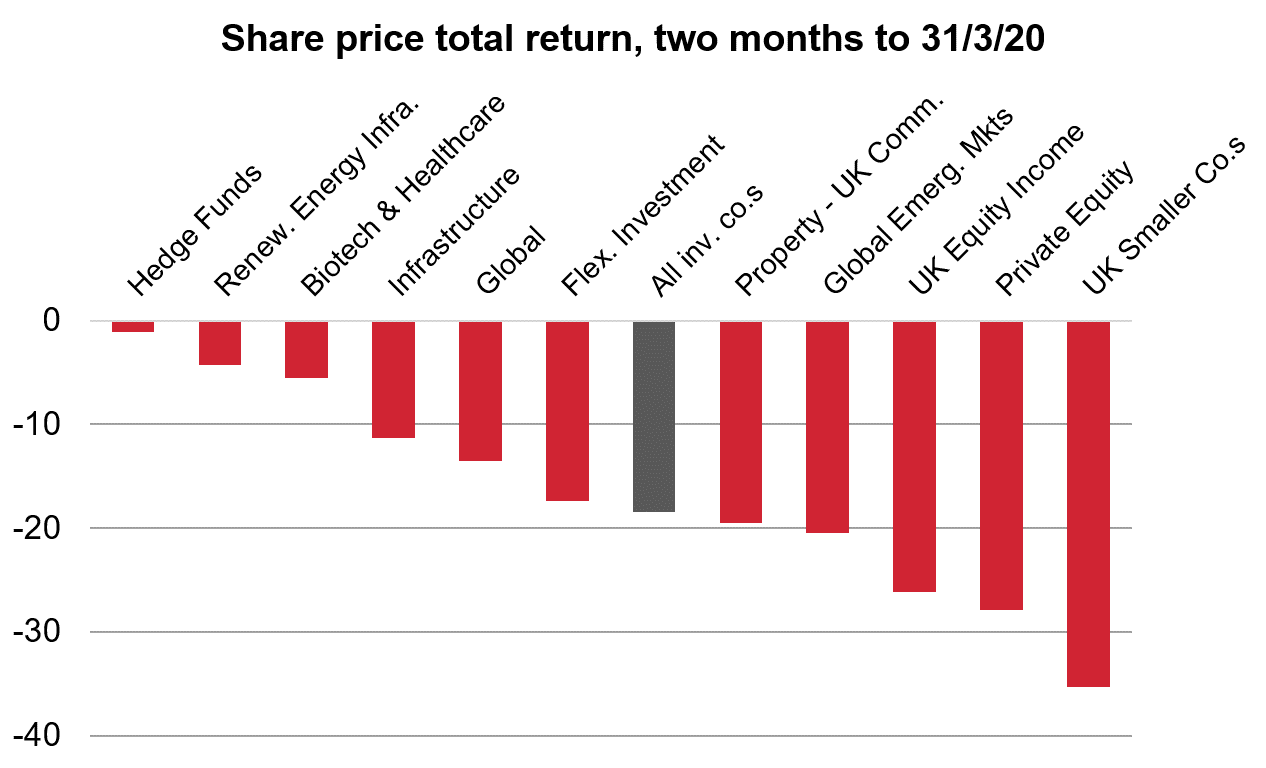

Since last month’s Spotlight, the longest bull market in history has breathed its last, brought down not by toxic debt or trade wars, but by a virus and the necessary measures to contain that virus. At times like this, it is good to hear from veterans of bear markets like Peter Spiller (38 years at the helm of Capital Gearing), Katie Potts (who has run tech-focused Herald Investment Trust for 26 years) and Austin Forey (celebrating his 25th anniversary as manager of JPMorgan Emerging Markets). We bring you all their views – and those of Asia expert Hugh Young – in this month’s Spotlight. How have investment companies fared during this most volatile of times? The average investment company has lost 18% of its value since the end of January. Every single sector is down over this two-month period, which began just after the WHO declared COVID-19 an international emergency.

The big equity sectors have fallen with the wider market, with Global down 14% and UK Equity Income down 26% in share price total return terms over the past two months. Private Equity is down 28%, while Property – UK Commercial has fallen 20%.

Source: AIC/Morningstar. (selected sectors)

The sector that has so far proved most virus-proof is Hedge Funds, serving its purpose as a diversifier (down 1%), followed by Insurance and Reinsurance Strategies (down 2%) and Renewable Energy Infrastructure (down 4%).

Fourth on the list is Biotechnology and Healthcare, which has lost only 6%. Its relative resilience is probably not surprising given that the current crisis has focused everyone’s minds wonderfully on how much we rely on these sectors to sustain our economy and way of life. Also this month, we bring you the thoughts of biotech and healthcare fund managers on the prospects for developing new vaccines, tests and treatments for COVID-19.

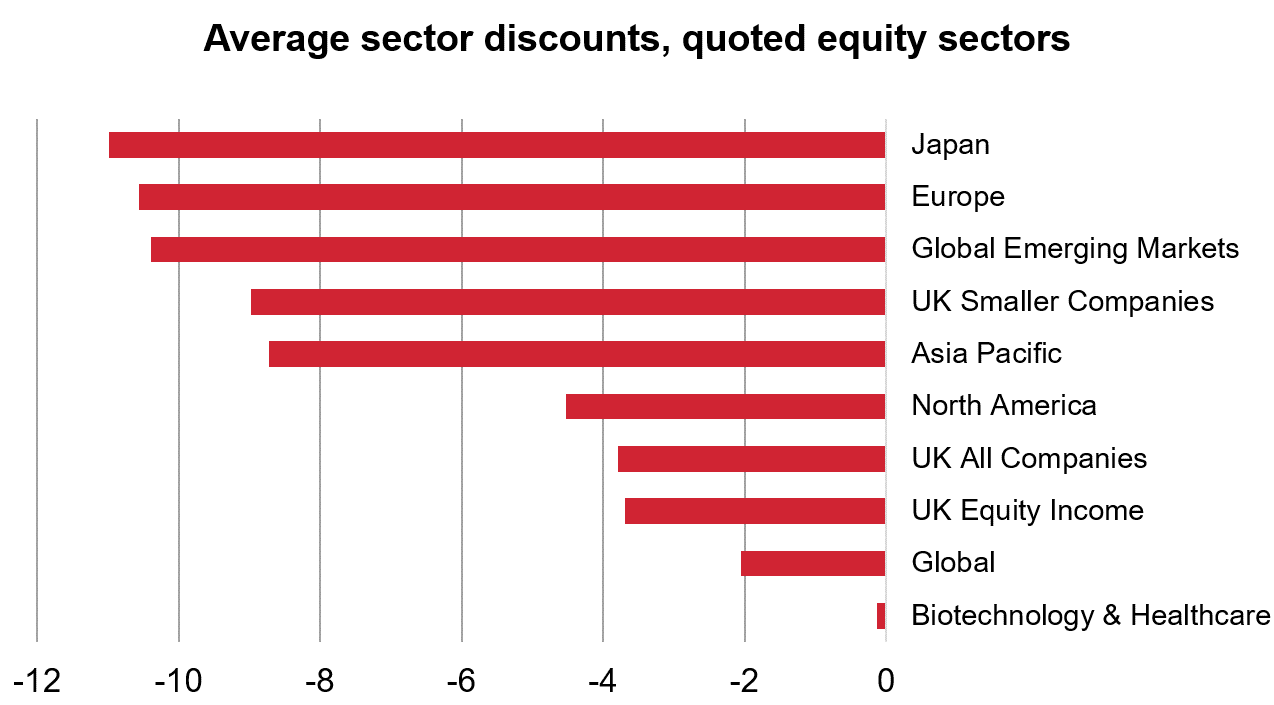

Source: AIC/Morningstar (as at 31/3/20)

Not surprisingly, the average investment company discount has widened over this period, from 4% at the end of January to 13% two months later. Discounts do tend to widen at times of market stress, and this is certainly one of those. Naturally, that widening discount will have accentuated the negative share price total returns just described.

While it may be tempting for investment company aficionados to treat these discounts as the industry equivalent of the summer sales, we need to be careful interpreting them for any sectors containing illiquid assets – now approximately a third of the investment company industry. The reason is that investment companies holding assets such as property, private equity and infrastructure do not produce daily NAVs: they may be monthly, quarterly or semi-annual.

This means that when we look at the discount of these investment companies, we are looking at the discount to a net asset value (NAV) that may predate the first UK coronavirus case, or even the WHO’s declaration of an emergency. The result is that the discount you’ll see quoted is somewhat wider than it would be, if the NAV was based on today’s valuations. To put this more bluntly, what looks like a screaming bargain at a 50% discount may not be, once we have factored in what the NAV is likely to be now.

Having said that, when we turn to the quoted equity sectors, it is perfectly possible to buy diversified portfolios of stocks, for the long term, at larger-than-usual discounts. Regional sectors have been fruitful hunting grounds, with the Europe and Japan sectors both on 11% discounts – though deep discounts are on offer within the mainstream UK and global sectors too.

So what is the ‘true’, bang-up-to-date NAV for a portfolio of unquoted companies, or physical properties? That is a very difficult question to determine, and if you want proof of that, have a look at the open-ended property sector, where the likes of Knight Frank and CBRE became so uncomfortable producing daily NAVs for the properties held in these funds that they had to (once again) suspend trading.

The truth is, of course, that we still don’t have much of a clue what’s going to happen with this pandemic. A mixture of social distancing and warmer weather could work wonders for bringing the virus under control, and we could all be back to work in a few weeks. Or at the opposite extreme, this could go on well into 2021, with waves of ‘false dawns’ (as we may already have seen in Japan) leading to the relaxation of lockdowns, only for those lockdowns to be reimposed later. We just don’t know.

So I completely understand why Knight Frank and CBRE have decided to spare themselves the heroic guesswork of estimating daily NAVs for open-ended property funds. I would still argue, of course, that it is better to hold a closed-ended property fund and be able to trade, albeit at a discount. But it’s yet another example of why daily redemption is an unrealistic proposition for property, a fact that the Bank of England, the FCA and the Investment Association now all seem to recognise.

We have recently released an updated list of our dividend heroes, the investment companies that have increased their dividends for at least 20 years in a row. Regular Spotlight readers will be familiar with the concept, and probably the names too: City of London, Bankers and Alliance Trust top the list with a track record of dividend-raising stretching back 53 years.

The dividend heroes have been tested before, and this will undoubtedly be another test of their ability to keep on raising dividends when income from their portfolio is set to fall. Only this week, the UK’s banks (including HSBC, a top holding in many equity income portfolios) announced the suspension of dividends. With the price of oil taking a drastic tumble, a question mark hangs over BP and Shell too.

The Winterflood team has analysed the 21 dividend heroes and finds that their median level of dividend cover is 129% - that is, sufficient revenue reserves to cover 15 months of dividends. It concludes that “the likelihood of any of these AIC dividend heroes not sustaining their dividend growth records is low at present”. Of course, there are no guarantees, and Winterflood does point out that the longer it takes for society to normalise, the harder these records will be to sustain. But it adds that favourable exchange rate movements are likely to help matters (with a falling pound increasing the sterling value of foreign income). There is also the ability to distribute income from capital profits – though for the vast majority of the dividend heroes this would be a notable departure from their long-established strategies.

This Foreword has been far longer than normal, but there’s a lot to say. The question of discounts and NAVs is particularly important – there’s been a lot of confusion about it already – and I thought it would be worth taking some time to explain it.

Very sadly, we’ve had to cancel all our face-to-face training events this spring, including our investment trust workshops. Our online training courses are still available (logged-in users can access them here) and we will be looking at ways to bolster our virtual offering.

Until next time, stay safe, stay well and don’t forget you can still contact me with all your investment company queries. Whatever you ask, it can’t be harder than my son’s latest poser: “Why don’t horses have hands?” Still pondering how best to tackle that one.

Nick Britton, Head of Intermediary Communications, AIC