by Nick Britton

Nick Britton

As we make the first tentative steps towards a return to normality, I wonder how we’ll look back on this period of our lives? For some, the loss of loved ones will sadly dominate their memories. Others are facing job insecurity and worries about paying the bills. But for those fortunate enough to avoid these struggles, lockdown has not been an altogether negative experience.

Since I gave up the family car last year (who needs one in London?) and have avoided public transport, I have spent the last three-and-a-half months within a two-mile radius of my home. One consequence of this is that I have got to know my neighbours a lot better. One warm evening last week, a bunch of us got together on my front drive for a few drinks. We now have a WhatsApp group including four households and a tentative plan to extend this gradually down our street.

Of course, the million dollar question is to what extent these changes of behaviour, habit and lifestyle will simply revert to normal when COVID is no longer a threat. The key may be to separate those changes which are obvious aberrations (like London neighbours talking to each other) from those which are continuations or accelerations of previously existing trends.

Among these is what has been called the ‘reverse’ or ‘retreat’ of globalisation. Gervais Williams, manager of the Diverse Income and Miton UK Microcap Trusts, wrote a book on this theme back in 2016, the year Trump was elected and the UK voted for Brexit. Since then we have seen US-China trade wars and the weakening of global institutions such as the World Trade Organisation. The COVID-19 pandemic has encouraged this tendency to pull up the drawbridge on the rest of the world.

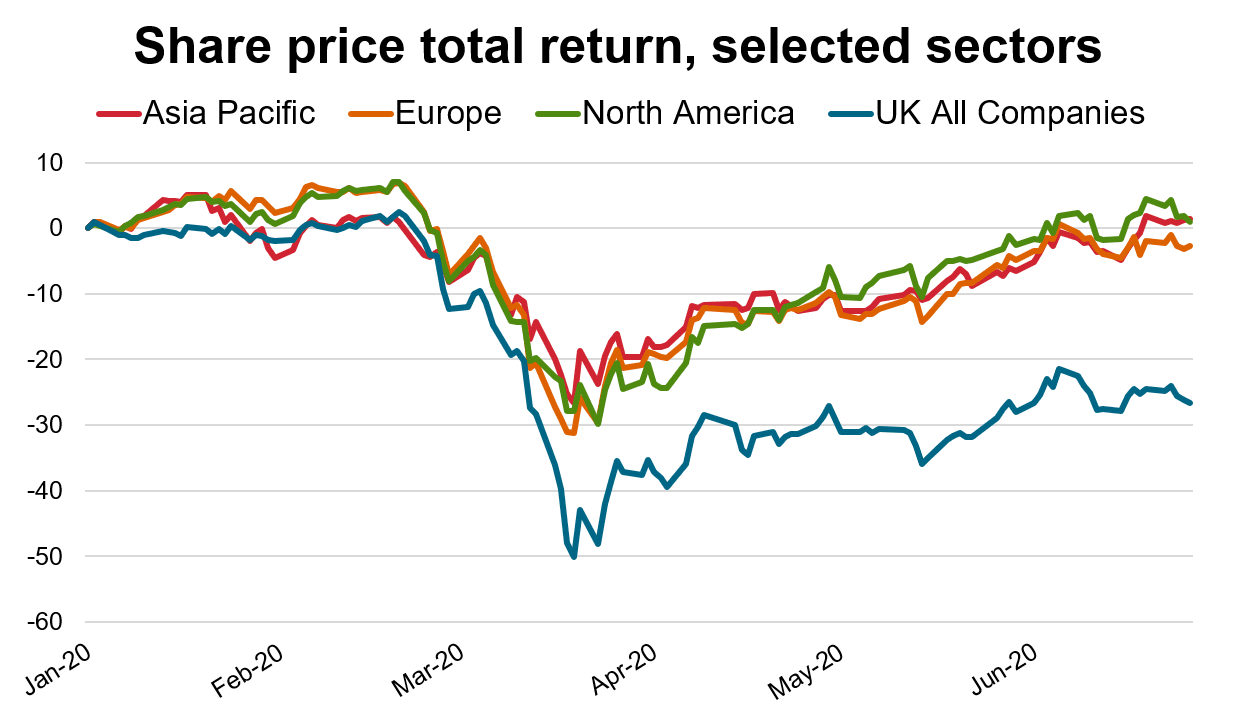

Source: AIC/Morningstar. Daily share price total returns from 1/1/2020 to 26/6/2020, AIC sector averages.

While these developments are often seen as clouds over the investment landscape, like the lockdown they could have their silver linings. Gervais believes that we are returning to a world more similar to the one he experienced when he started out in fund management in the early 1980s. At this time, he explained in an AIC media roundtable this week, there was no “tailwind” of stock market appreciation that investors could rely on. Institutions sought to improve their returns with meaningful allocations to smaller companies.

In contrast, he describes markets in the last 30 years as being like a dartboard “where you could hit anywhere and make money”. Allocations to smaller companies have dwindled because it has been enough to own the index. The retreat of globalisation holds the prospect of tougher markets where stock selection will become more important again. The UK, with its vibrant market of smaller quoted companies, could be well placed in this new world, where we will focus more closely on opportunities on our doorstep.

Hugh Young, manager of Aberdeen Standard Asia Focus, agrees that “globalisation has been the driver of the world in my career”. And he concedes that it’s had its excesses. But he sees the threat to globalisation as unhealthy: in his view, it will lead to the world becoming a more dangerous place. “Barriers are not a good thing, whether within a society or between societies,” he adds.

It’s entirely possible that Gervais and Hugh are both right, and that the retreat of globalisation will create both opportunities and threats. One thing seems more or less certain – it’s happening and it will have important consequences for our lives and our investments in future. You can read more views from Hugh, Gervais, and other fund managers focusing on Europe, the US and Japan, in this month’s Spotlight.

The reverse of globalisation is also set to impact levels of inflation. After all, globalisation has been one of the forces holding inflation down over the past few decades. We have gathered views of various investment company managers on the prospects for inflation (or deflation) and while there is broad agreement about the short-term outlook, with the impact of COVID being widely seen as disinflationary, the medium-term picture is more uncertain. Peter Spiller, manager of Capital Gearing Trust, points out that “once the crisis abates public debt will be at levels not seen since the Second World War”. He goes on to argue: “The solution to such problems will be the same now as then: financial repression, a prolonged period of low interest rates and elevated inflation.”

Not everyone agrees. According to Charles Luke, manager of Murray Income Trust, “Rising unemployment and the likely staggered recovery in consumption will weigh heavily on the outlook for wage and price growth. Fiscal and monetary policy stimulus should help cap some of these disinflationary forces, but are unlikely to fuel inflationary pressures over the next two years.”

Last week, shareholders in Scottish Mortgage voted to increase the investment company’s maximum allocation to unquoted companies from 25% to 30%. The increasing importance of private companies as part of the investment universe has been undiminished by the debacle at Woodford Equity Income last year. But they must be accessed using an appropriate structure. David Prosser rounds off this month’s Spotlight with a review of some research from Pantheon suggesting the advantages of an allocation to private equity.

Finally, I look forward to the first in our series of four webinars next week, Investment trusts explained. I know that many of you have signed up but for those who haven’t, there is still time to do so here.

Spotlight will be taking a break until September, so if you aren’t joining us for the webinars, I hope you have an enjoyable and relaxing summer.

Nick Britton, Head of Intermediary Communications, AIC

9-21 July - Investment trusts explained A series of four 45-minute webinars presented by Nick Britton that will explain all you need to know about investment trusts.